Tiny Market, Big Signals: A TINY Arb Story

There is a token called TINY. The name is almost too on the nose — and that is part of the point. In a lending stack where every basis point is a vote, TINY becomes a clean lens: not “which number is bigger,” but why two numbers can sit this close together and still mean different things.

The opportunity here is not a billboard. It is a whisper. The spread is small on purpose — and that is exactly what makes it interesting.

Two Thermostats, One Room

Picture two systems trying to keep a room comfortable.

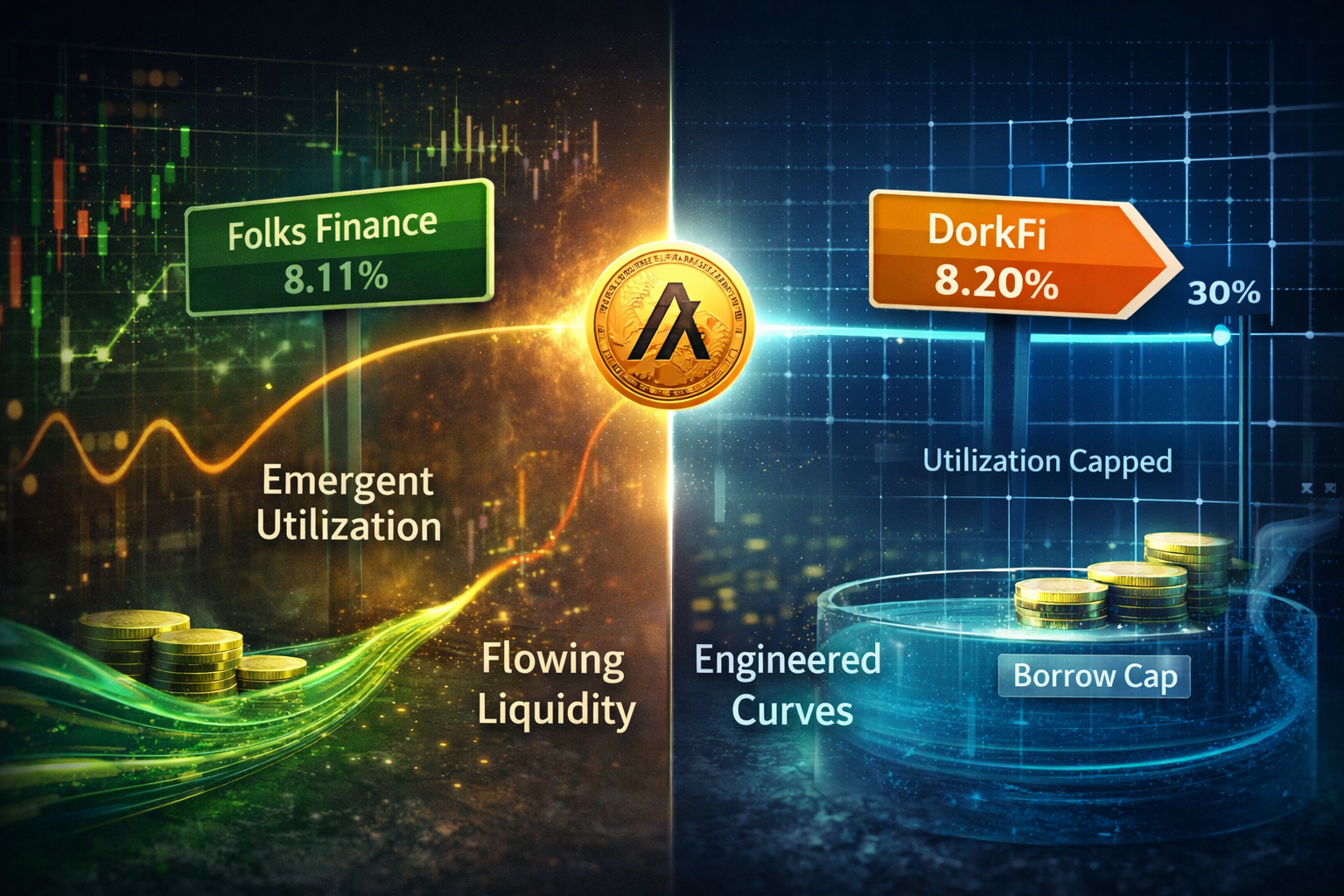

Folks Finance is running an isolated market for TINY with a supply APR in the neighborhood of ~8.11%. The yield is not handed down from a slogan; it is what the pool’s activity produces. Liquidity shows up, utilization wiggles, and the market prints a number that reflects the messiness of real use.

A DorkFi-style configuration aims closer to ~8.20% at the supply side — not because someone “likes 8.2,” but because the system is built to steer utilization toward a band where that outcome is the stable resting place. The knobs are different. The objective is different.

The gap between them is roughly ten basis points. On a spreadsheet, that looks like a rounding error. In protocol design, it is a fingerprint.

Small spreads are not noise. They are signatures of different control philosophies.

This Is Not “Extra Yield.” It Is Positioning

If you stop at “which APY prints higher,” you miss the plot. The meaningful split is not the tenth of a percent — it is what kind of market you are standing inside.

Emergent markets (Folks in this framing) behave like weather: incentives and flows collide, and the number you see is the atmosphere after the storm. Engineered markets (DorkFi-style) behave like climate control: caps, curves, and constraints exist so the system can defend a target state instead of merely recording whatever happened.

So when you allocate capital, you are not only choosing yield. You are choosing which feedback loop owns your exposure.

Three Arb Stories (Same Coin, Different Physics)

“Arbitrage” sounds like free money. Here it means pressure — capital routing until the easy edges close. Three sketches:

1) DorkFi under its utilization band. If engineered utilization is slack, the targeted supply-side print can look less compelling relative to an emergent pool that is simply “hot” with activity. Capital drifts toward Folks — not because Folks is “better,” but because the spread is the market’s blunt read on where liquidity is being rewarded right now.

2) DorkFi near its utilization ceiling. When the engineered system tightens, borrowing becomes the bottleneck and supply-side pricing can sharpen. Suddenly the same ten basis points read like a magnet: capital flows toward DorkFi because the constraint is doing what constraints do — reshaping who gets paid for taking which risk.

3) Borrow-side tension. If borrowers are the ones scrambling, routing pressure does not politely stay on one side of the book. Repay flows, re-leverage flows, and “where is it cheapest to roll?” become the hidden hands moving liquidity between systems — even when headline supply APRs look stable.

Borrow Cap = Strategy

Here is the clean mental model: a borrow cap is not a footnote in documentation. It is strategy made concrete.

Caps do not merely limit risk; they change the shape of the game. They carve out a bounded yield surface — the set of outcomes the protocol is willing to defend under stress. You can think of it like a tray with walls: liquidity sloshes, but only within contours the designers chose.

That is why two nearly identical APYs can imply opposite exposures. One is “what emerged.” The other is “what we are willing to let emerge.”

A Small Thought Experiment

Imagine Folks’ supply yield softens — not because the world ended, but because flows shifted and the emergent number drifted.

Now imagine DorkFi’s configuration holds its target band anyway, because the system is explicitly built to return to a designed equilibrium.

The arb is not “catch the dip.” The arb is recognizing that one line moved because the crowd moved, and the other line moved because the control system insisted. Same token. Different truth conditions.

Beyond TINY: Protocols as Control Systems

Zoom out, and TINY stops being a quirky ticker and becomes a tutorial.

DeFi protocols are increasingly competing as control systems: not only smart contracts, but the loops that govern how aggressively liquidity is solicited, how fast stress propagates, and how much discretion remains when users behave badly.

Caps, curves, and constraints are not “extra features.” They are primitives — the vocabulary protocols use to say: this is the world we are trying to keep stable.

Tiny Pun Section

The fees are tiny, but the drama is macro.

I’m not saying the edge is huge — I’m saying it’s TINY-but-mighty, which is a different kind of flex.

If you think ten bps can’t move markets, you’ve never watched liquidity do a tiny pivot at the wrong time.

And yes: the best trades sometimes come in small packages — just don’t confuse “small” with “simple.”

The Real Spread

The arb is not the 0.1%.

The arb is understanding why the spread exists — emergent versus engineered, weather versus thermostat, crowd print versus defended band. Capital is not chasing a number; it is chasing the story the number tells about who is in charge of the loop.

And when the signals align, money does not whisper — it moves.